Economic Outlook

Covid-19: gird up the loins

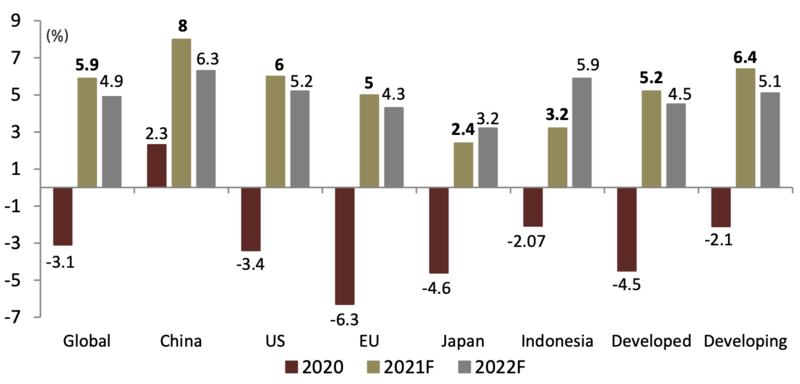

The face of normalcy has changed in unprecedented ways under pandemic. The number of lives taken now is almost 5 mn and the number of infections is already above 246 mn globally. However, the darkest hours have passed and the world is on track for stronger growth. The global economic growth is estimated to accelerate to 5.6% YoY in 2021 then slower to 4.3% YoY in 2022. Amid the hardships, Indonesia has been recovering and sustaining the 1-2 mn vaccine jabs per day to achieve herd immunity in 1H21. Besides the progress of Covid-19 handling, US tapering would be anticipated in 2022. However, recovery is widely believed to happen in 2022.

- SEA chutzpah stepping into 2022

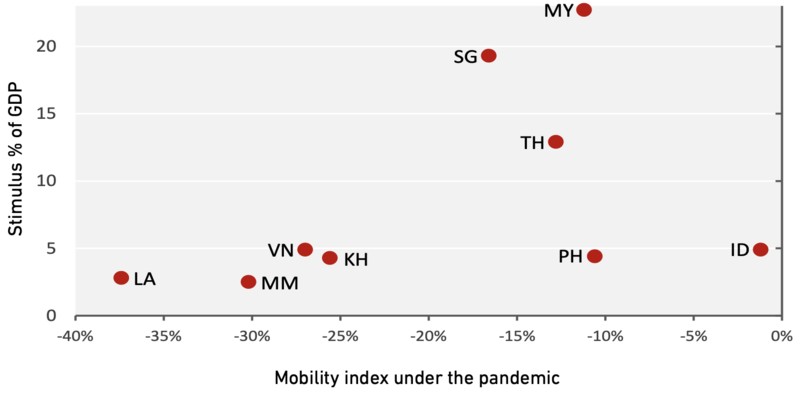

The Delta variant brings the deadliest wave of Covid-19 cases in Southeast Asia (SEA) where it has been reaching 5.4% of global death due to Covid-19. Besides, the pandemic exacerbated political unrest in some SEA countries. However, SEA has been putting the pandemic under control and welcoming the SEA normal growth approximately 5% YoY in 2022. With around 35% of vaccinated population, SEA is ready to do reopening economy in 2022 while it is used to with reimposition of stringent Covid-19 containment measures. Compared to others, Indonesia mobility almost goes back to normal condition. With the similar fiscal commitment like in 2021 and people adapting to the lockdowns, SEA is very optimistic to have economic recovery in 2022.

- Struggling for pre-pandemic level

Herd immunity is achieved by vaccinating 181 mn people by early 2022 where the current progress is at 33.5% of Indonesian has got their first jab. As the game changer, vaccine enables Indonesia to bounce back. In 2021, the government expects 3.7-4.5% YoY of economic growth then it will jump to 5.5% YoY in 2022. However, we maintain our view that Indonesia economic growth will be at 3.5% YoY in 2021 and jump to 4.9% YoY in 2022 as the domestic demand contributing 54% of GDP has not gone back yet to the normalcy.

Exhibit 1: Global Economic Growth Forecast

Source: IMF

Exhibit 2: Covid-19 handling in SEA

Source: Google Mobility Report, Ciptadana estimates

Interest rate: more hawkish

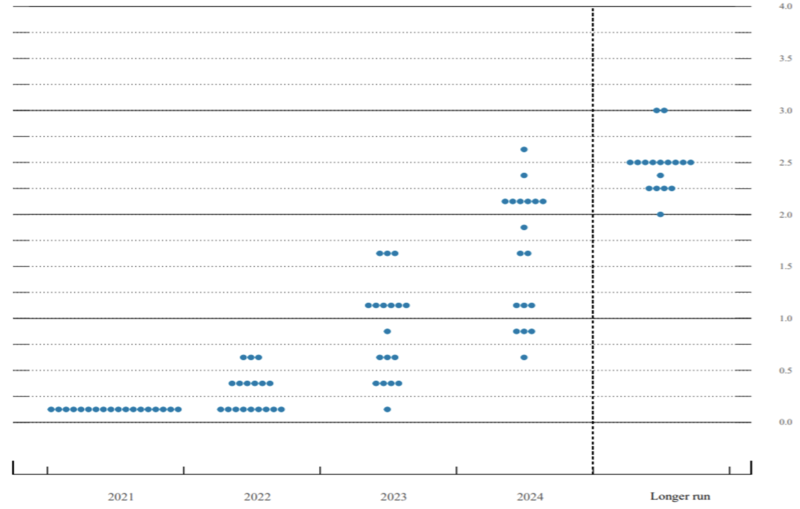

The labor market seems to have slower recovery but the demand stays high lately. Combined, both of them create inflationary pressures. In response, the Fed’s dot plot projection shows uptrend starting in 2022 to curb the rising inflation. The Fed has penciled in a rate increase to 0.25-0.50% in 2H22. The projection itself is never set in stone as it may evolve regarding what future holds. However, it triggers worldwide interest rates to go slightly higher.

As response to the pandemic, BI has cut BI-7DRRR by 150 bps to 3.5% and injected liquidity worth more than USD57 bn. However, in general, monetary policy is less effective than fiscal policy amid the still-weak demand side. Besides, as long as the inflation remains low and the exchange rate remains stable, current BI rate is preferable. Thus, we expect BI will increase the rate at least one time by 25 bps to 3.75% in 2H22 without ruling out the possibility of it reaching higher level because BI use wait-and-see approach towards the Fed.

- More accommodative monetary policy

BI expands more accommodative policies with probability to be extended until 2023. To spur the credit distribution, BI maintains looser down payment requirements on automotive loans/financing at 0% until Dec-22. Property sector also gets relaxation on its LTV/FTV ratio to a maximum of 100%. BI also extends minimum payment policy on credit card at 5% of the outstanding balance until Jun-22. In addition, many local currency settlements (LCS) are also enhanced to facilitate more bilateral business to come.

- Extended burden sharing to 2022

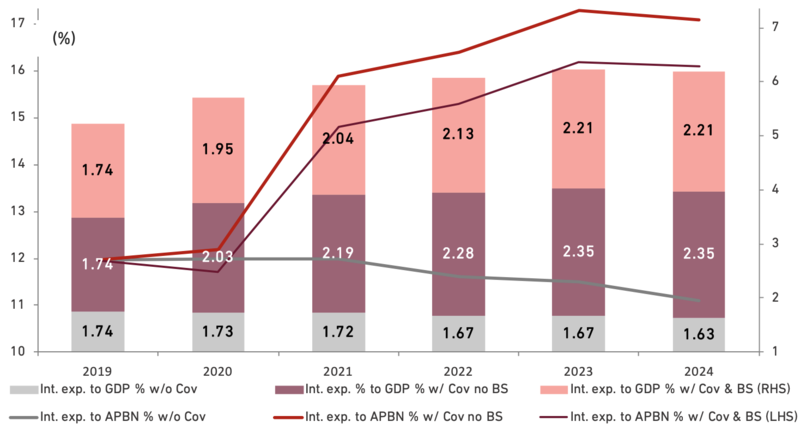

Ministry of Finance (MoF) and BI extended the Joint Ministerial Decree (SKB) III regarding burden sharing mechanism until Dec-22. BI will buy Rp439 tn (USD30.5 bn) worth of government bonds (SBN) in the primary market and private placement. The decree is divided into 2 clusters: (1) Cluster A: financing vaccinations and health care with a maximum limit of Rp58 tn in 2021 and Rp40 tn in 2022; (2) Cluster B: financing community and MSMEs various protection programs up to Rp157 tn in 2021 and Rp184 tn in 2022 but the government will bear the interest expenses for Cluster B.

Exhibit 3: FOMC dot plot projection

Source:The Fed

Exhibit 4: Interest expense to state expenditure under BS scheme

Source: MoF, BI

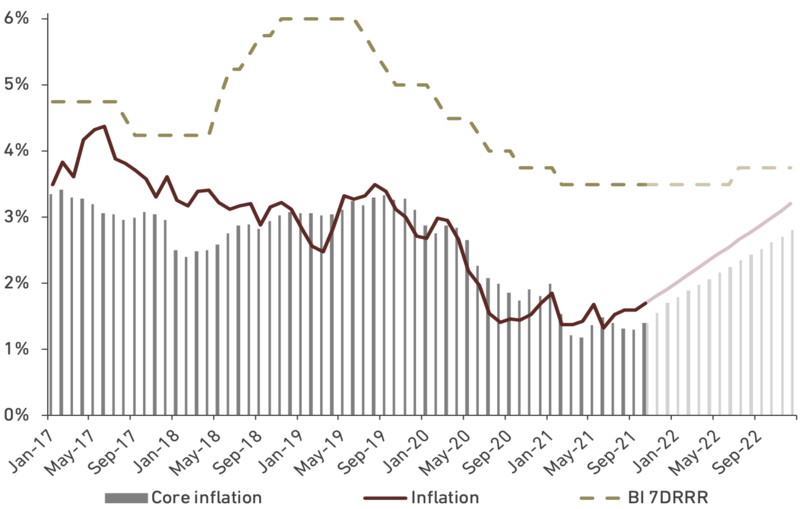

Inflation kicks in manageably

The various mobility restrictions in Indonesia are responsible for the muted inflation during pandemic. With decreasing cases and higher vaccination rate, the mobility restrictions will be less strict so domestic spending can go back normal. Alongside, the stronger domestic demand and the soaring world commodities prices will bring higher inflation in 2022. BI predicts the inflation rate will be at 2-4% YoY in 2022. We expect inflation to stay low at 1.9% YoY in 2021 as households still tend to be frugal. After the economic recovery becomes bolder, we expect it will be at 3.2% YoY in 2022.

Global energy prices soared in 3Q21 and we see it will persist to 2022, revising up OECD global inflation rate forecast from 3.5% to 4.3% YoY in 2022. Some commodity prices have exceeded their highest level since the spike in 2011 such as natural gas and coal. This will benefit Indonesia as an energy-exporting country. However, we expect supply side will normalize and the demand will not face any significant growth unlike in 2021. We also expect anomaly on inflation contributors where under the pandemic, contribution of foods is not the biggest. Internally, a spike in some set of prices: food, energy, airfare, etc. will happen because of the disruptions on supply and the looser mobility restrictions. However, it is still manageable as we expect the core inflation will only achieve 2.8% YoY in 2022.

- Anticipating imported inflation due to tapering

It is widely believed that the upcoming Fed tapering will likely to be less severe than its impact in 2013. However, we are anticipating the downside risk of the tapering to the exchange rate where it may create volatility in the beginning (approximately in 4Q21 and 1H22). In the weaker exchange rate period, Indonesia may face imported inflation where a fall in the exchange rate will also raise import prices. This is significant to domestic manufacturers as the import of raw material/intermediary goods is 75.5% of total import. It is only about a time the higher price borne by the producers will be translated into higher price on consumers. Especially, producer price index (PPI) has been soaring consistently since beginning of 2H21 due to the rising raw material costs. We expect the rising PPI will be followed by the consumer price index (CPI) as the correlation in past 10 years shows lag for about 3 months.

Exhibit 5: Inflation and policy rate estimates

Source: BI, BPS, Ciptadana estimates

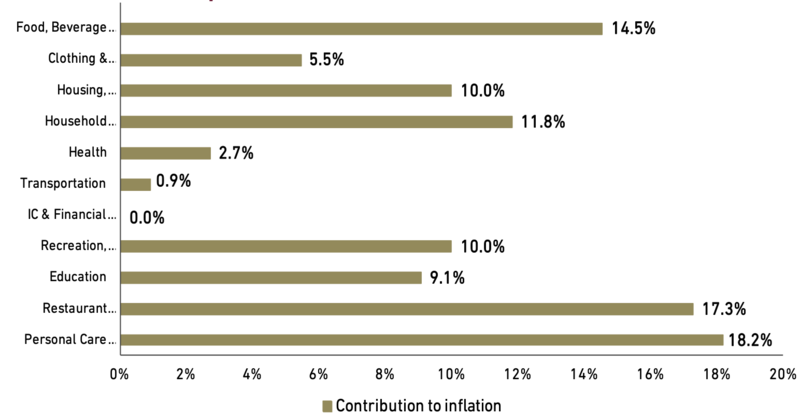

Exhibit 6: Inflation components contributions in 2021

Source: BPS, Ciptadana estimates

Resilient external sector

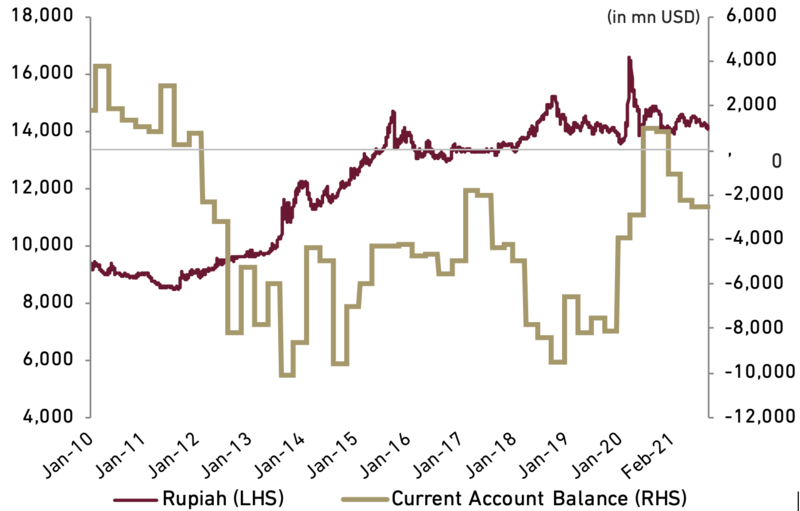

Since late 2011, Indonesia recorded current account deficit (CAD) until it reversed to surplus in 3Q20. In 1H21, CAD was recorded relatively low at USD3.29 bn (0.6% of GDP). The CAD is relieved due to the jump trade surplus since the beginning of 2H21. Commodity prices surge played significant role due to the growing demand from energy-importing countries due to the energy crunch. We expect trade surplus will likely help to narrow the CAD in 2H21. However, the more relaxed mobility restrictions in 2022 may boost domestic consumption, as a result, demand of import increases. Therefore, the current account balance will go deeper as we expect from the relatively low at -0.9% of GDP in 2021 to -2.1% of GDP in 2022.

- Natural deficit in current account

With the financial account balance has not gone back to its normal balance around USD28 bn in average since last 5 years, we see the primary income will not go back to its normal balance around USD30 bn. Thus, we see the CAD will be relatively low as well. However, we see there will be a big potential on portfolio investment inflows (65% of the financial account) as foreign investors’ risk appetite can go higher in 2022 under the recovering economy. As the economy recovers, the deficit will go back slowly to its natural deficit to around 2% of GDP in 2022 and afterward if Indonesia still heavily exports raw material and depends on imported processed commodity.

- Mega surplus in trade balance

It has been a 17th straight month of trade surplus and we expect the surplus will remain until YE 2021. In Aug-21, Indonesia recorded the all-time high trade surplus at USD4.74 bn from the highest surplus at USD3.57 bn since Aug-11. We expect the surplus may achieve around USD33.1 bn in YE 2021 due to the previous mobility restrictions creating weak demand for imported goods. After surging on the back of commodity prices boom in 2H21, we expect the commodity price will go lower in 2022 as the supply side will recover, deteriorating Indonesia trade performance as commodity is around 60% of our exports. Further, domestic consumption and manufacturing sector become stronger in 2022, creating thin trade deficit as we expect the import will grow at 6.1% YoY, higher than the export growth at 5.2% YoY in 2022.

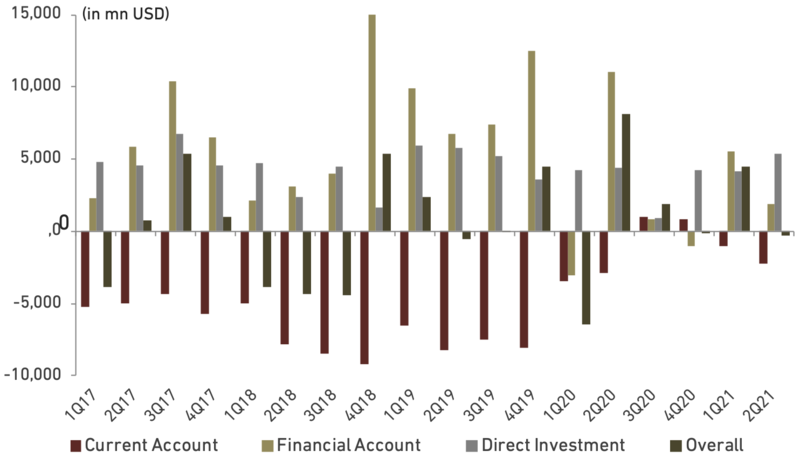

Exhibit 7: Balance of payment

Source: BI

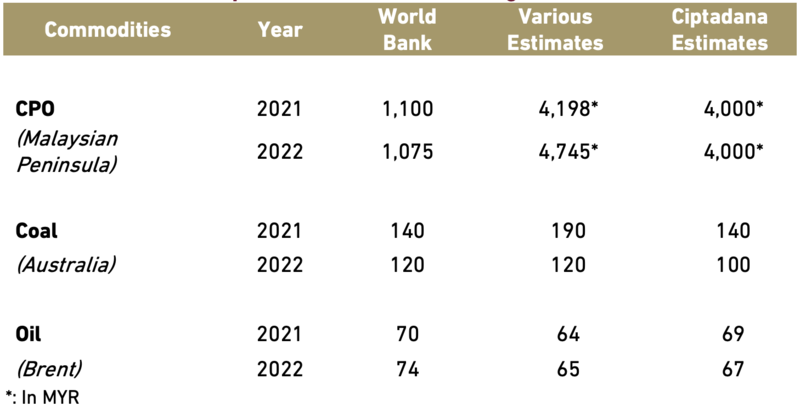

Exhibit 8: Commodities price forecast (annual average)

Source: WB, OECD, Trading Economics, Ciptadana estimates

More stable exchange rate

In 2021, Indonesia exchange rate ranges from Rp13,914 in Feb-20 to Rp14,634 per USD in Apr-21. Despite the better prospect of the US economy, rupiah has been steadily appreciating to around Rp14,200 to Rp14,300 on the back of the better domestic Covid-19 handling, higher commodity prices and high foreign exchange (forex) reserves. BI predicts rupiah will hover at Rp14,200 - Rp14,600 per USD in 2021 and 2022. We expect in YE 2021, rupiah will reach Rp14,318 and appreciate more to Rp14,285 in YE 2022 as the economy is getting more conducive. Nevertheless, the currency volatility will follow the development of Covid-19 cases in Indonesia.

The previous massive government bond-buying program strengthens the currency and bond yields. However, MoF mentioned that it would reduce the bonds issuance because the bonds issuance has already achieved 47% of the State Budget target of Rp1,207 tn (USD85 bn) in Aug-21. In 2022, MoF also plans to lower bonds by 0.2% YoY to Rp991.3 tn (USD69.8 bn). Besides, MoF wants to utilize the remaining budget surplus (SiLPA) from 2020 which still remains Rp234.7 tn (USD16.5 bn). The reduction is done wisely as the state revenue is increasing more than expected in Sep-21 where it has achieved 71.5% of the target in 2021. Meanwhile, the state expenditure slipped by 1.9% YoY achieving 65.7% of target in the same period. We expect the state revenue may achieve more than 90% of the target as tax revenue usually spikes at the end of the year.

- Less but stable foreign exchange reserves

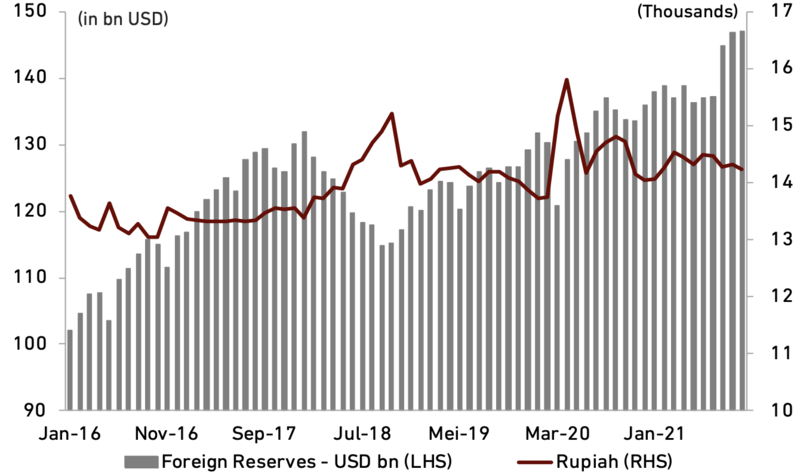

In Sep-21, the forex reserves were at an all-time high at USD146.9 bn supported by the tax and services receipts during commodity boom and the government’s external debt withdrawal. With the thick forex reserves, BI has sufficient ammunition to support the exchange rate if US yields rise further during the tapering. Due to the lower bond issuance and the lower trade surplus ahead, we expect the foreign reserves will slip slightly in 2022 to maintain the debt ratio manageable. It has reached Rp5,971 tn (USD423.5 bn) or 37.2% of GDP in Aug-21. We see MoF will limit the debt ratio not to reach 40% of GDP in 2022 as it raises the risk of weakening macroeconomic stability.

Exhibit 9: Rupiah and current account balance estimates

Source: Bloomberg, BI

Exhibit 10: Rupiah and forex reserves

Source: Bloomberg, BI

Fiscal policy under the pandemic

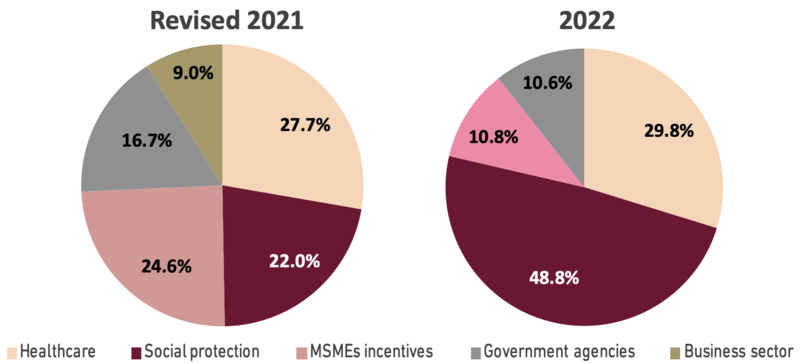

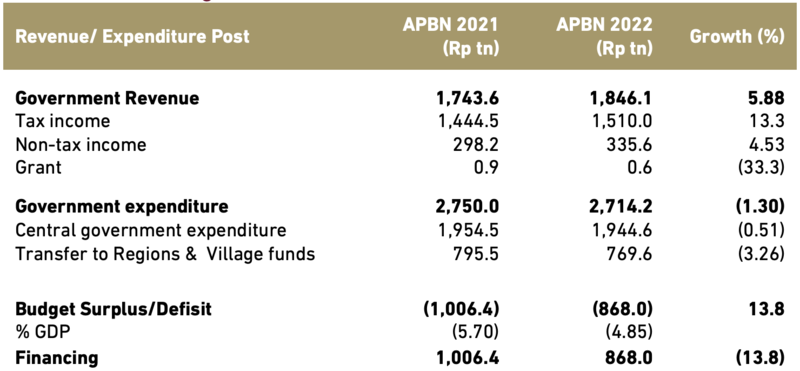

To enhance the economy, the State Budget for 2022 was designed to support the economic recovery. It includes state revenues of Rp1,846.1 tn (USD129.9 bn) and state expenditures of Rp2,714.2 tn (USD191 bn), resulting in a deficit of Rp868 tn (USD6.11 bn) or 4.85% of GDP. As much as Rp744.8 tn (USD52.6 bn) is allocated for National Economic Recovery (PEN) program 2021 and Rp321.5 tn (USD22.6 bn) for 2022 to cushion the impact of the pandemic. It comprises stimulus for: 1) social protection (2021: Rp186.6 tn & 2022: Rp126.5 tn), 2) MSMEs incentives (2021: Rp162.4 tn & 2022: Rp27.9 tn), 3) healthcare (2021: Rp214.9 tn & 2022: Rp77.1 tn), 4) priority programs (2021: Rp117.9 tn & 2022: Rp27.5 tn) and 5) business incentives at Rp59.4 tn in 2021 without any 2022 allocation. Realization of the stimulus is underperformed as it has only reached 58.3% in Oct-21. However, we see the low absorption as a happy problem. It implies that the healthcare cost is lower than expected due to the decreasing Covid-19 cases lately. Probability of reallocation is wide-open due to its flexibility anyway.

- Fiscal priorities in 2022

The state expenditure in 2022 is set at Rp2,714 tn (USD191.6 bn) or 15.1% of GDP. By having “Economic Recovery and Structural Reform” as fiscal policy theme in 2022, MoF allocates 7 priority sectors: (1) health at Rp255.3 tn (9.4% of state expenditure), (2) social protection at Rp427.5 tn (15.8%), (3) education at Rp541.7 tn (20%), (4) infrastructure at Rp384.8 tn (14.2%), (5) information and technology at Rp27.4 tn (1%), (6) food resiliency at Rp76.9 tn (2.83%) and (7) tourism at Rp9.3 tn (0.34%). The unprecedented fiscal support to mitigate the pandemic also put a huge burden in State Budget as MoF has allocated Rp405.9 tn (10.8% YoY) on debt interest payment next year.

- Maximizing potential revenue in 2022

The state revenue in 2022 is set at Rp1,846 tn (USD130.3 tn) or 10.3% of GDP. Under the new Taxation Harmonization Law (UU HPP), it can boost the tax ratio from 8.44% to 9.22% to GDP in 2022. Gradually, the tax ratio can achieve 10.1% to GDP in 2025. Under the law, the value added tax (PPN) will be at 11% in Apr-22 for 2 years then climbs to 12% in Jan-25. Tax Amnesty II in Jan-Jun 2022 and addition of a 35% personal income tax (PPh) rate subjecting those with an annual income over Rp5 bn may realize the potential revenue next year.

Exhibit 11: Share of stimulus to total PEN allocation in 2021 and 2022

Source: Coordinating Ministry of Economic Affairs

Exhibit 12: State budget for 2021 and 2022

Source: MoF

Anchoring on the domestic consumption

Indonesia has crawled out from the recession in 2Q21. Thanks to the stronger household consumption that grew by 5.93% YoY, it contributed as much as 55.1% of GDP. Despite of the hardships during pandemic, according to BI’s consumer survey, people tend to increase their spending reflected from the average propensity to consume ratio that increased to 75% in Aug-21. The saving to income ratio also decreased from 15.1% to 14.6% in the same period. We see the Consumer Expectation Index increases whenever the mobility restrictions are eased. By having more optimistic consumer ahead, we expect the household consumption can grow by 3.1% YoY in 2021 and bounce back to its normal rate at 5.0% in 2022.

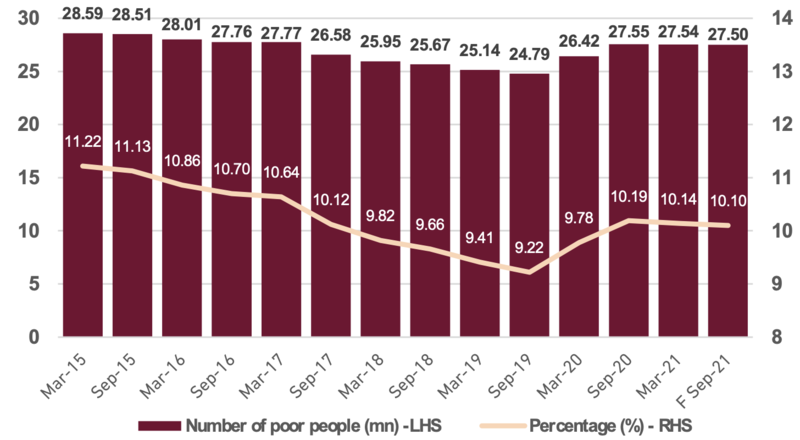

Uneven recovery patterns lead to worsening inequality. The poor people are bearing the brunt of the pandemic through liquidity shortages and job losses. However, since 2021, the government has mitigated the widening depth of poverty so the poverty rate decreased by 0.05% to 10.14% in Mar-21 through some programs. The social protection programs consist of (1) Family Hope Program (Rp28.1 tn), (2) food assistance card (Rp45.1 tn), (3) education assistance program (Rp20.7 tn), (4) National Health Insurance program (Rp46.5 tn), (5) electricity subsidy (Rp56.5 tn), (6) LPG subsidy (Rp66.3 tn), Pre-Employment Card (Rp11 tn), (7) microfinance credit (KUR) interest subsidy (Rp23.1 tn), (8) village cash transfer (Rp27.2 tn) and others like the new Job Loss Insurance. By having it all, we expect the poverty rate can go lower again to 10.1% in Sep-21 and henceforward. This is important as investment in the people is a prerequisite for rapid growth.

- Meanwhile the haves save more

In 1Q21, there was an increase in income as reflected in the 14.4% QoQ of increase of PPh 21 tax revenue. However, the higher income of the upper middle class is not allocated for consumption expenditure which is expected to stimulate the economy of people in the lower class. They tend to allocate their income to face future uncertainty through financial products. This is indicated by the increase in savings (3.19%), equity (54.83%) and mutual funds (52.78%) on quarterly basis in 1Q21. We expect the consumptive spending pattern will go back whenever the government eases the mobility restrictions ahead.

Exhibit 13: Number of people living under poverty rate

Source: BPS, Ciptadana estimates

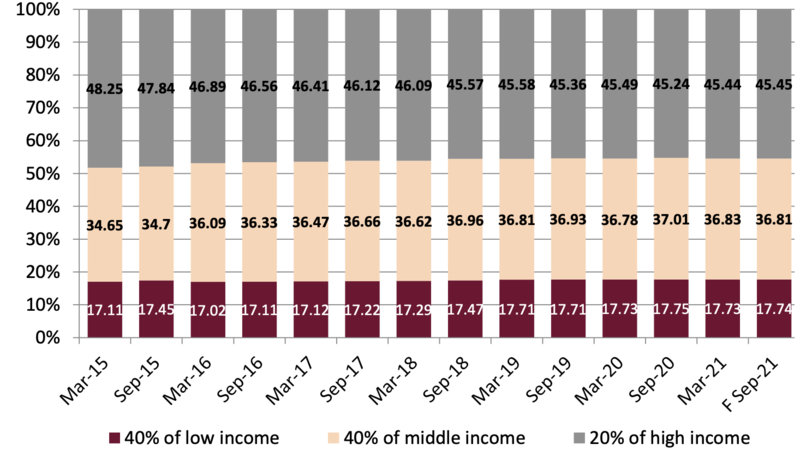

Exhibit 14: Share of household spending

Source: BPS, Ciptadana estimates

Investment as cusp of significant growth

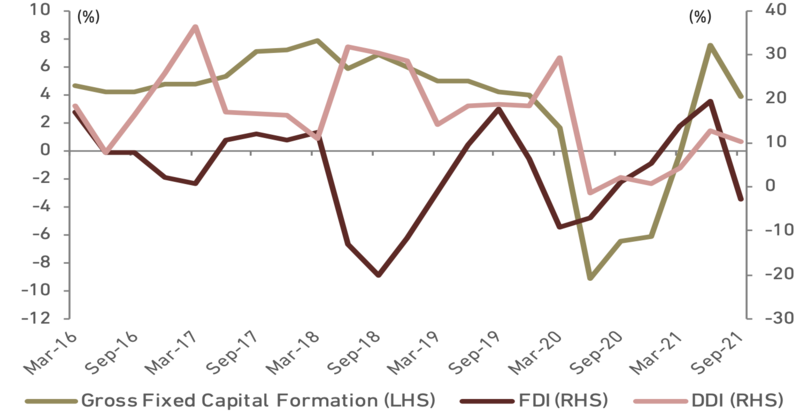

While the consumption cushions the economy from falling down deeper, investment leads the economic growth rocketing in 2Q21. In Jan-Sep 2021, the investment realization was at Rp659.4 tn (USD46.3 bn) or grew by 7.8% YoY (vs 1.7% YoY during Jan-Sep 2020). For domestic direct investment (DDI), it reached Rp331.7 tn (49.7%) and foreign direct investment (FDI) reached Rp327.7 tn (50.3%). There were 83,786 investment projects that absorbed 912,402 workers. It reached 73.3% of the 2021 investment target mandated by President Jokowi at Rp900 tn. We expect the target could be achieved as last year target was surpassed by 101.1% during harder momentum than 2021. The impressive result is coming as the investment climate is getting robust.

- Institutional reform to attract investment

Through the establishment of a “one stop shop” for risk-based licenses and permits via online single submission (OSS) system by Ministry of Investment (MoI), it will simplify the process of doing business. The government also removed Negative Investment List so it increased the inclusivity of investment. MoI also has identified an over USD400 bn infrastructure spending need over 2020-2024 where Indonesian Investment Authority (INA) can carry this out. INA was also established to attract foreign equity and long-term investment to finance infrastructure projects with daring target of USD200 bn in the next 2-3 years. Besides, special task force of MoI is running to attract more foreign investors, especially those who have left China during the pandemic.

MoI has set ambitious target of investment realization at Rp1,100 tn in 2022. To increase the value added, investment on manufacture sector will be pursued. It will be more inclusive as well because MoI has included a list of 145 business fields that have to form partnerships with Micro, Small and Medium Enterprises (MSMEs). As we are still under a low policy rate regime, we see it will be easier to attract investment in 2022 as the cost of borrowing is at the lowest. With stable and longer-term source of foreign flows, it will surely support the macroeconomic stability in long run. We expect the gross fixed capital formation (GFCF) can boost the economic growth by growing at 4.3% YoY in 2021 and jump at 5.3% YoY in 2022.

Exhibit 15: GFCF estimation and FDI-DDI realization

Source: BPS, MoI, Ciptada estimates

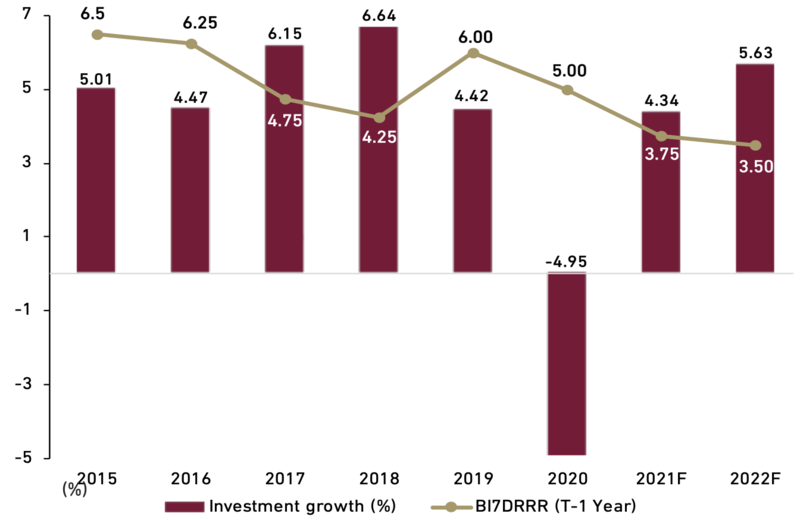

Exhibit 16: Investment growth and BI-7DRRR

Source: BPS, BI, Ciptadana estimates

What to expect

Adverse impact of US tapering is the main topic in 2022. We are optimistic that in the short run, there is no threat. Compare to the previous US tapering in 2013, Indonesia is standing on different ground now. Indonesia is no longer heavily subsidizing the fuel like in 2013. However, the possibility of tantrum happening is still there. Dealing with tantrum can be very draining but giving up is not an option. The response to it is not to give the pacifier all the time, but embracing the tantrum and being calm. Above all, macroeconomic forces are cyclical; this too shall pass.

Indonesia has been appointed as the 2022 G20 Presidency that will be held in Nov-22. G20 presidency would foster economic effects considering there will be about 150 meetings and side events throughout 2022. With “Recover Together, Recover Stronger” theme, we hope the momentum will spur international investors’ confidence on Indonesia. The government has to utilize the opportunity to showcase its success in structural reforms through the Job Creation Law and the establishment of INA. As the most impacted in terms of economic growth, Bali, where the G20 meetings will be held, will have its come back moment, supporting the national economic growth as well.

- Pot of gold at the end of rainbow

We have survived the great calamities by getting out of recession in 2021. However, the scar needs more time to heal. Next year will determine whether Indonesia can go back to the pre-pandemic level or not. The K-shaped recovery has been vanishing as the most damaged sectors are already recovering. Facing the Fed tapering and some high-leveraged corporate debt crisis like Evergrande will be crucial for Indonesia economy but as far as we are concerned, the adverse impact is scanty in 2022. There are actually some silver linings like the shift from bond market to stock market as big funds tend to avoid potential systemic risk in bond market due to the particular corporate debt crisis in China. In 2023, the government will push the budget deficit to below 3% of GDP, creating limited fiscal booster. Furthermore, 2024 election year comes alongside with its positive impact for economic growth from higher domestic consumption as the main driver. Thus, the good is coming.

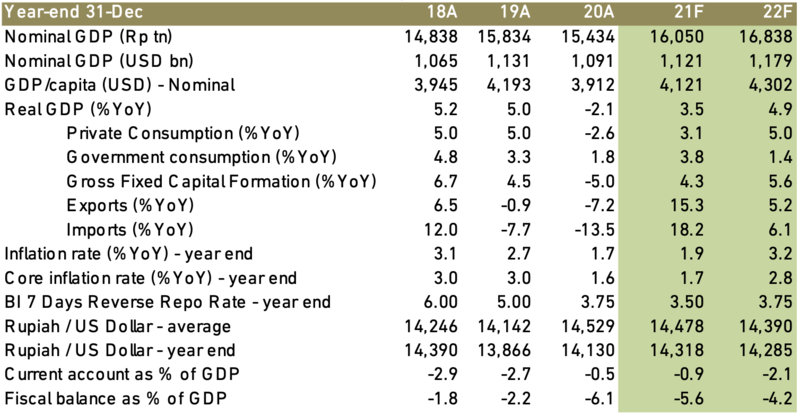

Exhibit 17: Indonesia’s Macroeconomic Projection

Source: BI, MoF, BPS, Ciptadana estimates